[ad_1]

With the Federal Reserve promising to keep the Fed Funds rate at 0% or close to 0% for years, it’s good to think about potential inflation on the horizon. Specifically, we should learn about investments that can hedge against inflation and also benefit from inflation.

If our income and our investment returns are not beating inflation each year, on a relative basis, we are losing. Therefore, it is up to each of us to at least keep up with inflation.

My annual net worth growth target is 10%, which is on average, 5X higher than inflation. 10% was relatively easy to beat when I had a day job before 2012. Now, it’s relatively harder to beat with similar risk exposure. But I won’t stop trying because I’ve now got a family.

The following is a post about investing as a hedge against inflation by FarmTogether, a leading farmland investing platform and dedicated Financial Samurai sponsor.

Investing As A Hedge Against Inflation

Inflation is an unavoidable reality. The purchasing power of cash has a direct bearing on the value of your holdings—market volatility can make it hard to get a true and stable sense of how much your portfolio is worth.

A robust financial strategy means hedging against downside from as many angles as possible. Inflation might not be the first risk factor one might think of when minimizing investment downsides. However, inflation can be a crucial factor in maintaining the value of your overall holdings.

Depending on how you choose to hedge against inflation, you may even open yourself up to an investment that does more than just safeguard assets.

The multi-fold tactics available to hedge against inflation can create unique opportunities to do more than just outpace inflation. Let us explore in more detail.

How Inflation Affects Investments

The exact level of inflation is difficult to predict, but it easy to identify. The hallmarks of inflation: shrinking unemployment, rising wages, and increases in commodities and raw materials can all influence the likelihood of an upcoming inflationary period.

When inflation hits, its impacts on the economy are multifold. The costs associated with lending increase, purchasing power decreases, and consumer confidence takes a dive.

Depending on your portfolio, some or all of these phenomena could negatively impact your investments. Investors looking to grow their long-term purchasing power have a hard road ahead when inflation hits. More generally speaking, an inflationary period can provide you with fewer opportunities to maximize growth and, in some cases, reduce your overall portfolio’s purchasing power.

Inflation doesn’t impact all investment types equally, however. Those with fixed, long-term cash flows see a diminished return as far as purchasing power is concerned.

On the other side, commodities and other products with a cash flow that ebbs and flows, tend to fare better during inflationary periods.

Why It’s Important To Hedge Against Inflation

If, like most investors, your goal is to maximize your rate of return. Doing so also means trying to earn a rate of return as far above the inflation rate as possible.

A high level of inflation creates a “tax” on capital. The tax must first be paid before a corporation can produce any real return for its shareholders.

The Tapeworm Of Inflation

As Warren Buffett once said,

“Inflation acts as a gigantic corporate tapeworm. That tapeworm preemptively consumes its requisite daily diet of investment dollars regardless of the health of the host organism. Whatever the level of reported profits (even if nil), more dollars for receivables, inventory and fixed assets are continuously required by the business in order to merely match the unit volume of the previous year.

The less prosperous the enterprise, the greater the proportion of available sustenance claimed by the tapeworm. The tapeworm of inflation simply cleans the plate.”

How High Inflation Affected Stocks In The Past

Inflation in America was highest in the 1970s. However, the worst stock performance of the 1970s came when inflation first spiked, not when inflation peaked.

From 1972 to 1973, inflation doubled to more than 6 percent. By 1974 inflation rose by another 5 percent to 11 percent. In those two years, the S&P 500 declined by a combined 40 percent.

By the time inflation topped out at 13.5 percent in 1980, the S&P 500 had returned to positive territory. However, on an inflation-adjusted basis, the 1970s showed no real returns for stocks.

To help increase the chances of beating inflation, equity investors should focus on companies with strong cash flow and pricing power.

How Inflation Affects Fixed Income

Fixed income investments tend to struggle during periods of accelerating inflation as well. When inflation is rising, a bond’s fixed-rate payment loses its purchasing power.

Further, the Federal Reserve tends to increase its Fed Funds rate in a high inflation period to combat inflation. As a result, fixed income investments become relatively less attractive because they are paying a relatively lower rate. A fixed income investment may decline in value to the point where its yield is competitive to competing fixed income investments.

Investments That Can Hedge Against Inflation

The best way to help safeguard against inflation is to allocate funds into financial products whose value is not tied as closely to increases and decreases in purchasing power.

Investments that also provide dividends irrespective of market performance can also provide a hedge against inflation’s impact on market performance.

These assets can offer a degree of resiliency where other investments may not. Better still, several of them may even provide dividends and payments to shareholders as well.

Precious Metals, And Commodities

Some of the most common strategies for hedging against inflation include buying gold, silver, grain, or even orange juice. These are only a few of the many commodities that can hold their value against inflation.

When purchasing power declines, these items tend to hold their value. Many become even more valuable as they become harder to afford.

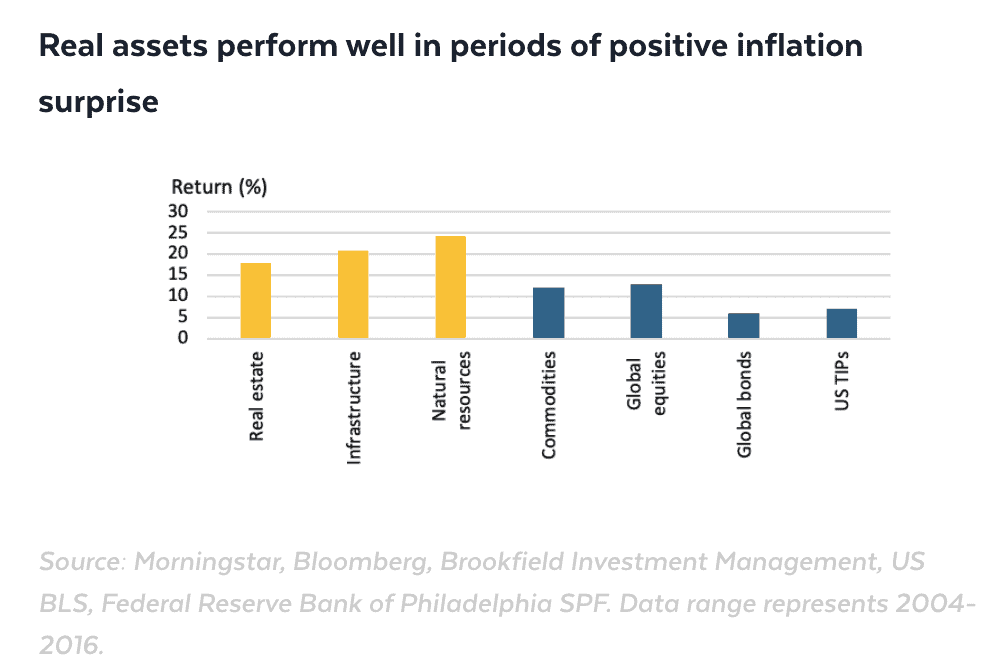

Below is a chart that shows how real assets perform during periods of positive inflation surprise. Natural resources, infrastructure, real estate, and commodities perform the best while bonds perform the worst.

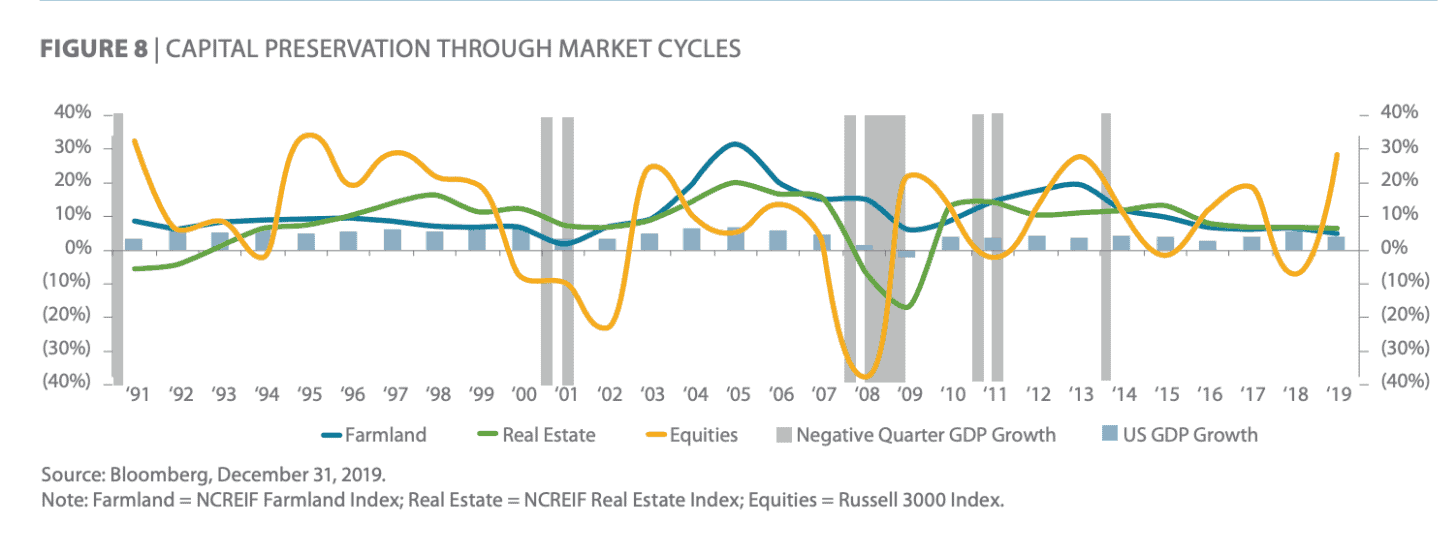

Below is a chart that shows the asset return characteristics from 1970 – 2018. Notice how US farmland had the highest annual average return of 10% with a relatively low standard deviation of 6.5%.

Meanwhile, the NASDAQ had a similar annual average return of 9.7%, but a much higher standard deviation of 24.6%. In other words, investing in the tech-heavy NASDAQ is much more volatile.

Real Estate As An Inflation Play

Real estate tends to ride the inflation wave rather than get hurt by inflation. In other words, the demand for real estate outweighs the cost of higher mortgage rates.

Landlords tend to be able to charge higher rents in a high demand, inflationary environment. As a result, real estate values increase.

At the same time, rental properties tend to get more valuable in an ultra-low interest rate environment where there is minimal inflation because the value of rental income goes up. It takes more capital to produce the same amount of risk-adjusted income.

As one of the foundations for survival, real estate is one of the best performers in almost any type of inflationary environment.

Farmland Investing As An Inflation Play

Investing in precious metals, commodities, and REITs are all popular options for hedging against inflation. However, the more popular these options are, the relatively more expensive they become.

Farmland investing, on the other hand, offers an excellent option as a hedge against inflation.

With farmland, you’ll get returns from land appreciation when you sell as well as annual cash income from the crops. Farmland’s value rises at least as fast as inflation for good reason. Because of what it creates – food.

Food is the third-largest category used to calculate the Consumer Price Index, or CPI, one of the two most common measures of inflation. Like real estate, food is a necessity for all households. Out of an average $82,852 household income, roughly 10% is spent on food.

That means inflation is in part calculated based on the price of key commodities. Then as food – or if you own farmland, crop – prices rise, then those changes are reflected back in inflation.

This alternative investment is one of the most attractive asset classes, on a risk-return basis. Historically, agricultural land has demonstrated little correlation with traditional asset classes, such as stocks and bonds. This quality makes farmland a desirable addition to any portfolio looking to enhance diversification and seeking to lower volatility.

Invest In Farmland With FarmTogether

With FarmTogether—the preeminent institutional investment team in the space—you can benefit from the expertise that comes from a team of financial pros who curate investment opportunities with a target return of anywhere from 7 to 13 percent and 3 to 9 percent cash yields.

One of the other advantages FarmTogether offers qualified investors is the ability to make small commitments. As an accredited investor, you’ll only need $10,000 to get started. You will see a myriad of investment opportunities across agricultural products and locations throughout the country.

Hold periods are as short as five years, and investments come with annual liquidity windows for exiting earlier. Fees are low, and the FarmTogether site lays out all of the specifics of the opportunity, ranging from cash yield, target hold, offering size, and target IRR within an intuitive and data-rich interface.

Anticipating inflation can be a tricky endeavor. Hedging against inflation doesn’t have to be. FarmTogether offers a major hedge against inflation while offering a unique investment opportunity that other common investments can’t. Sign up to hedge against inflation and potentially benefit from inflation with FarmTogether here.

[ad_2]